The stablecoin market should have consolidated by now. Payments are textbook network-effect territory: scale lowers cost, deepens liquidity, and attracts more users, which further lowers cost. Yet the opposite dynamic persists in stablecoins. Despite more than $250 billion outstanding and trillions in annual volume, we’re seeing more issuers, more designs, and more jurisdictional variants—not fewer.

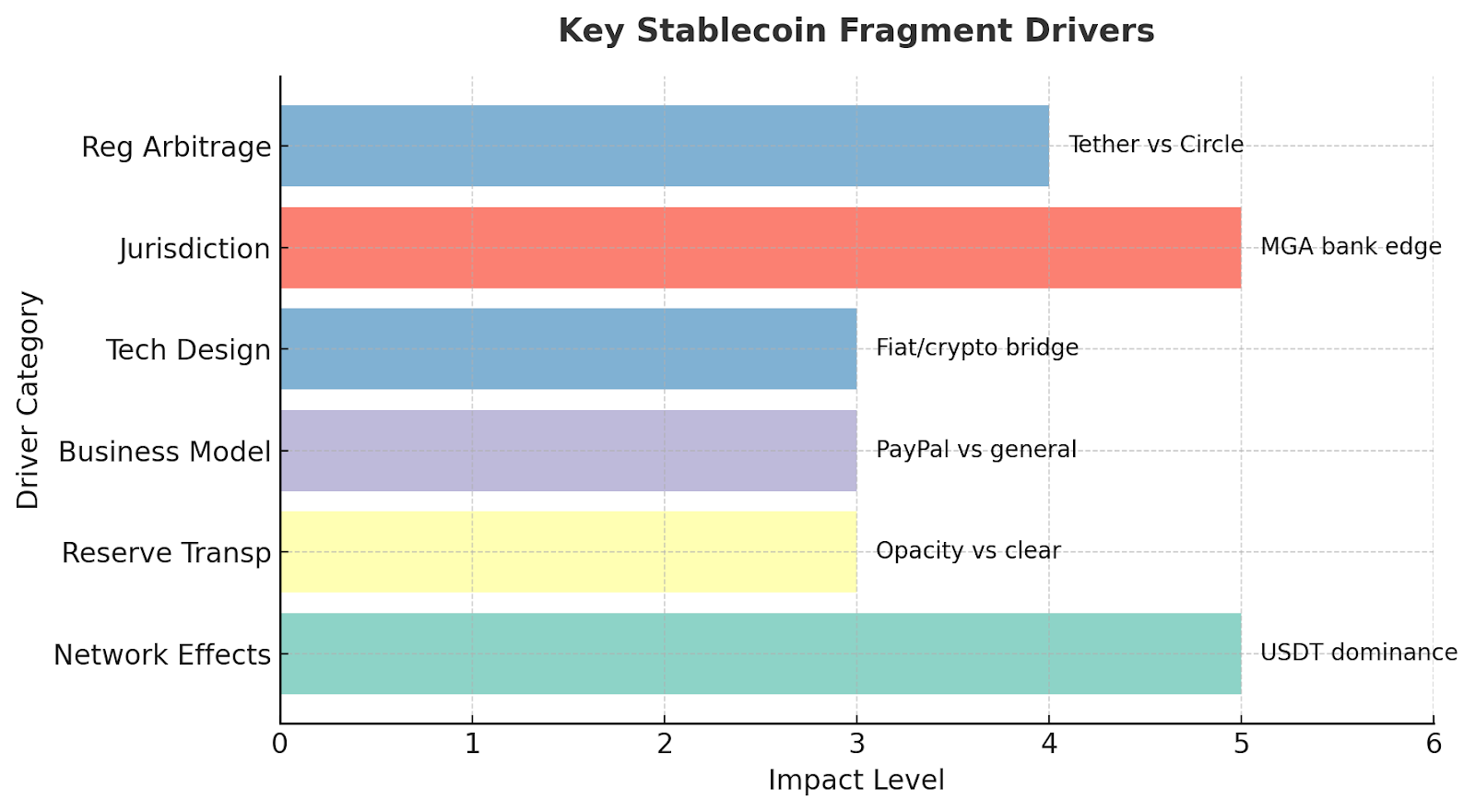

Fragmentation endures because incentives and constraints cut across pure network effects. Regulatory arbitrage remains the central engine: issuers optimize for domicile, licensing pathways, and supervisory posture, creating distinct regulatory clusters with real competitive edges. Some prioritize lighter oversight and speed-to-market; others trade pace for compliance credibility and institutional access. Technical differentiation compounds this: fiat-redeemable tokens, crypto-collateralized designs, and algorithmic approaches speak to different risk tolerances. Multichain deployment and ecosystem specialization—Solana-first, EVM-first, or a broad multi-chain stance—further segment liquidity, particularly when bridges introduce security and operational risk that discourages seamless flow.

Business models diverge in ways that reinforce these boundaries. Certain issuers lean on reserve income to subsidize fees; others monetize enterprise-grade APIs, transparency, and servicing. Distribution paths also differ: integration with payments rails drives one adoption funnel while DeFi-first integrations drive another, and the two are only partially overlapping. Underneath it all, use cases themselves are specialized. Trading collateral and emerging-market remittances do not resemble regulated settlement or enterprise treasury needs. The token that wins one domain is structurally disadvantaged in another.

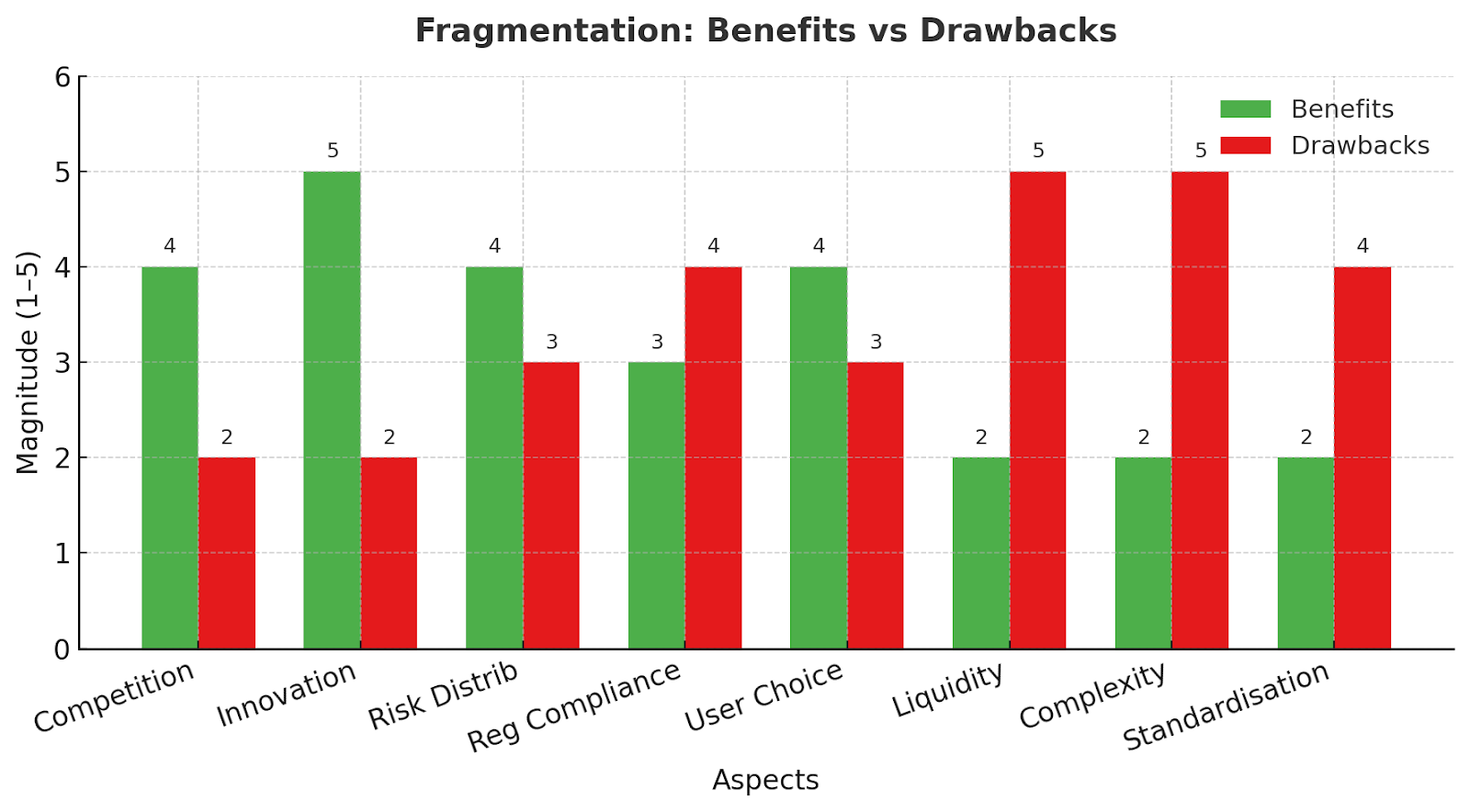

The costs of this fragmentation are real. Liquidity is scattered across tickers and chains, widening spreads and increasing slippage—especially during stress. Cross‑chain movement adds latency and security overhead, which blunts arbitrage and slows the compression of dislocations. The user experience degrades as well. Multiple tickers, issuers, KYC stacks, and wallets create friction for mainstream users and complexity for merchants. Institutions pay a compliance tax to underwrite each token and jurisdiction before they can participate at scale.

Yet fragmentation also buys the market valuable real options. Competitive pressure pushes fees lower, redemptions faster, attestations tighter, and reserve reporting more transparent. Systemic risk is diversified because a single issuer shock—or a single bank exposure—doesn’t automatically cascade when credible substitutes exist. Parallel innovation flourishes in this environment: collateral models, programmability features, and privacy primitives can be tested in market without putting the entire category at risk.

Where does this lead? The most likely outcome is selective consolidation rather than monoculture. Expect a handful of major ecosystems to dominate by region, regulatory perimeter, or use case, with long‑tail specialization persisting at the edges. Consolidation forces include payment network effects at scale, economies in reserve and compliance operations, and gradual regulatory harmonization that narrows today’s arbitrage window. Countervailing forces—geopolitics around monetary sovereignty and CBDC adjacency, continued technical breakthroughs that open new niches, and distribution moats tied to incumbent platforms—will keep the market plural.

What deserves to be built in this world is abstraction. The winning infrastructure reduces user‑visible complexity while preserving competition under the hood: aggregated wallets, unified liquidity routing, safer cross‑chain movement, and policy frameworks that set baseline standards without freezing design space. The aim isn’t to erase fragmentation; it’s to make it productive.